This week’s Brexit news was overshadowed by the chaotic end to 20 years of Western occupation of Afghanistan. A lot has been written about this historic episode. Some see the retreat as a symbol of the decline of US hegemony, although others contradict. Unsurprisingly, commentators who see ‘neoliberalism’ as the cause of all evils, even express some satisfaction over an event they see as signalling the end of ‘neoliberalism’ (although their explanation is neither conceptually nor chronologically convincing).

Domestically, the event has exposed once again the incompetence and recklessness of the Johnson government and this time in particular the Foreign Secretary. More importantly though, the key implication of the fall of Afghanistan to the Taliban is that five months after the publication of the Integrative Review of Security, Defence, Development and Foreign Policy, which fleshed out Johnson’s ‘Global Britain’ strategy, that strategy has already been exposed for what it really is: yet another slogan without any substance. The US retreat from Afghanistan and the other Western countries scramble to evacuate their nationals has exposed Johnson’s claim as Foreign Secretary that Britain was back ‘east of Suez’ as another illusion of grandeur, which would only ever have an ounce of credibility if the US were to militarily support that presence. The US’s uncompromising retreat from Afghanistan shows that the UK cannot count on the US any more than any other NATO member state – let alone non-member states. That leaves the UK terribly isolated now that it has chosen not to rely on its closet neighbours anymore. The horrific events in Afghanistan are another real-world event that expose Brexiteers’ perception of the UK’s role in the world for what it is: A great illusion.

The Brexit of little things

In the Brexit of little things category, we continued to receive various news stories this week about food shortages. Nandos announced that it had to close 45 restaurants due to shortages, which the BBC squarely blamed on the pandemic – not mentioning Brexit with one word. This interpretation was explicitly dismissed by people in the poultry industry. Avara Foods – a large UK poultry producer – and the head of the British Poultry Council both denied the industry had been affected by the ‘pingdemic’ and underscored instead that ‘the UK workforce has been severely depleted as a result of Brexit.’

Other Brexit of little things news, that even the BBC had to attribute to Brexit, concerned a story about thousands of UK exchange students still waiting for their visas to spend a year in Spain.

International trade according to Brexiteers

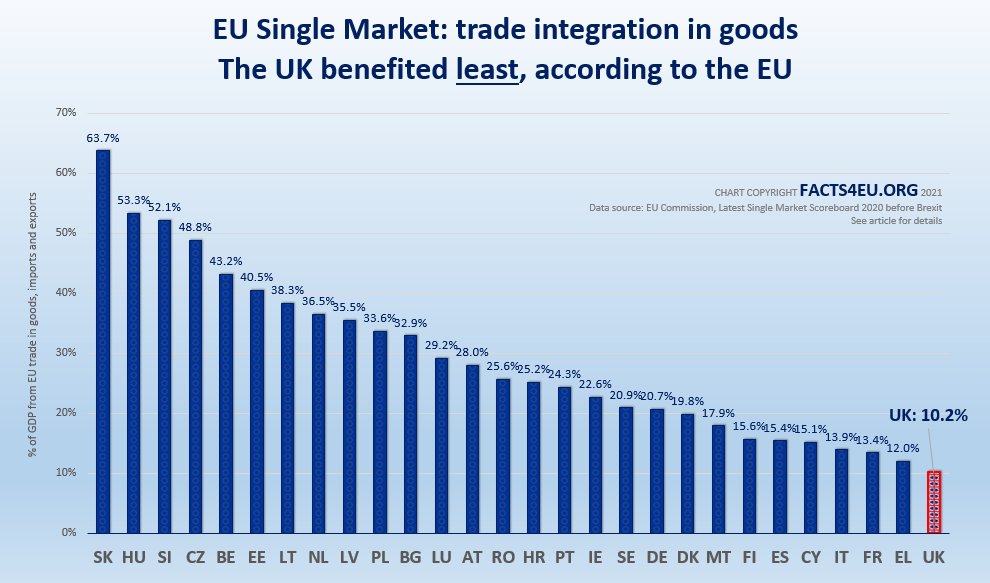

But this week’s price for the most bad-faith article on Brexit goes to Facts4EU (and the Express) for a report on the latest EU Single Market scoreboard.

The web site sees the Brexiteer’s cause confirmed by the fact that the latest edition of the scoreboard ‘ranks UK bottom, at No.28 out of 28 EU countries’ and that therefore – using a fake quote attributed to the EU – ‘UK benefited least from our greatest achievement.’ So, the Remainers’ arguments in favour of the staying in the Single Market have been ‘debunked.’ Tory MP John Redwood is even quoted as seeing the results as confirmation for the conspiracy theory that ‘[t]he single market was designed against us and promoted continental exports to us to replace our home production.’

What’s wrong with this interpretation of the scoreboard exercise? Several things.

It is true that the scoreboard concluded that in 2018 “[t]he UK [had] the lowest trade integration in the Single Market for goods and the third lowest trade integration for services.” What that means is that the value of trade in goods and services with other EU member states as a percentage of GDP was lower for the UK than for virtually all other EU countries. Facts4EU have created these nice little graphs for trade in goods and services to illustrate that.

{kind=link}

{kind=link}

Facts4EU interprets these results as not just a bad thing – which is also the EU’s interpretation of the figures, as higher levels of trade integration are uncritically seen as a good thing – but also a sign that the EU exploited the UK somehow. These claims need debunking.

Firstly, looking at the countries at the top of the rankings (to the left of the graph) we find Slovakia, Hungary, Slovenia, and the Czech Republic as the top four. All of them are post-socialist new EU member states. Why do they have such high levels of single market integration? The main reason is that after the fall of communism these countries together with Poland, relied heavily on foreign companies to help them upgrade their industrial capacities and bring them to international standards. This happened to a large extent through foreign direct investment (FDI) by German manufacturing companies, especially in the automotive sector. Many German manufacturers set up shop in East Central Europe to take advantage of the low wages and the relatively highly skilled workforce. Much of the production in these – small – countries were meant for export to the rest of the EU, which explains the reliance on imports and exports.

Now, if being to the right of this chart means ‘bad for your country/economy’ as Facts4EU suggests – then being to the left should be really good news for these countries. Partly that is true. The Visegrad Group (Hungary, Poland, Czech Republic and Slovakia) and to some extent Slovenia too, were amongst the most impressive success stories of post-socialist transition in terms of modernising their economies and integrating into the European and world markets. However, these countries have recently seen sever political turbulences with two of them (Hungary and Poland) on track to become authoritarian regimes according to many observers. This trend has in turn be explained by political scientists – like Doro Bohle – by the exhaustion in the late 1990s of welfare payments to compensate those who did not benefit from the economic modernisation. Trade figures, only provide a very one-sided picture of the health of a countries economy and – more importantly – the prosperity of its population.

Moreover, political scientists Andreas Nölke and Arjan Vliegenthart have coined the term ‘Dependent Market Economies’ (DMEs) to describe the Visegrad countries. In fact, they almost exclusively had to rely on foreign investments to upgrade the largely outdated technology inherited from the socialist period, making them dependent on investment decisions taken by companies based outside their national borders. In other words, being more to the left of the graph may be interpreted as higher dependence on the EU. So, in another example of the twisted logic behind Brexit, Brexiteers now advance the fact that the UK was not as dependent on the EU market as other EU countries, to argue that leaving was the right thing to do, when they were complaining about being too dependent on EU while we were a member.

Secondly, if we look at the countries next to the UK in the chart you see smallish Mediterranean economies (Greece and Cyprus), but also some of the EU’s other large economies, namely France and Italy which have only slightly higher levels of trade integration than the UK (13.9% for Italy, 13.4% for France, compared with 10.2% for the UK). So, are France and Italy equally the victims of an EU conspiracy to ‘hold them back’?

One thing to note here is that percentage of export and import by GDP will almost naturally be higher for small countries than large ones. If we take the 5 most integrated countries to the left of the chart, we find they have a combined population of 39m (using Wikipedia figures), while the 5 least integrated ones to the right have a combined population of 205m – and that in spite of the fact that these five include Cyprus that has a population of less than 1m. So, being a large country almost necessarily leads to lower levels of integration. Why? Because large countries have large territories, large populations, and large internal markets, which makes them – all else equal – less reliant on imports and exports than small countries. So, the position of the UK in the ranking does not seem that different from other large EU member states.

Thirdly, another dishonesty hidden in the Facts4EU analysis of the Scoreboard is the fact that it only looks at the figures for trade inside the EU. If you scroll down on the EU’s web page to ‘facts and figures,’ you can see that UK intra-EU imports (i.e. imports from other EU countries) are 12.4% of GDP, but extra-EU imports are 10.4% of GDP. Similarly, exports to the EU are 8% of GDP, exports to countries outside the EU are 8.3% of GDP. Given that the EU is a much smaller region than the rest of the world, this illustrates that the UK did depend disproportionately on trade with EU members. In fact, if we just focus on exports here and assume that exporting is an unmitigatedly good thing for a country (which is a discussion for another day), the UK benefits as much from trading with the 27 EU members than from trading with the other 167 countries in the world (there are currently 195 countries in the world).

Brexit impact on FDI

Another dishonesty in the Facts4EU analysis is that – interestingly – the article only focuses on trade in goods and services and not on investments, which the EU also analysis.

Here the EU figures for 2018 show a ‘remarkable increase in [the UK’s] intra-EU FDI outflows, and a significant decrease in its intra-EU FDI inflows.’ In other words, two years after the referendum, the value of new investments by UK-based firms in other EU member states has increased, while the value of EU member states new investments in the UK have decreased. Why might that be? One argument would be that anticipating a hard Brexit and new trade barriers, UK-based firms had an incentive to start setting up shop inside the Single Market (SM). Conversely, the uncertainty about the UK’s status after Brexit will have put off investments from the continent (e.g. because firms did not know if tariff free exports back into the EU would still be possible).

The FDI figures also provide clues as to how the UK did benefit from SM membership: While the UK lost out in 2018 in terms of new investments from the EU into the country, the figures on the value of FDI stocks (the value of accumulated investments already made in the country) was the third highest in the EU after the Netherlands and Luxemburg (scroll down to the figure Inward intra-EU FDI stocks – levels). Of course, if inflow of FDI from within the EU continues to evolve in the direction it went since 2016 (The figure “Inward intra-EU FDI flows – levels” shows that between 2016 and 2017 inward FDI from the EU dropped by 75% and was negative by 2018) – and from outside the EU close to zero (see figure ‘Change in inward extra-EU FDI flows’), that picture may soon change and provide a striking example of a real loss from leaving the SM.

There is a deeper truth that the Facts4EU’s interpretation of the Scoreboard reveals about how Brexiteers think about trade: Like everything in the Brexiteer’s universe, trade is a zero sum game. What others win you lose. What you win others have to lose. That is how Brexiteers approach national and international politics, trade, and economic activity in general. This attitude explains to a considerable extent why in the Brexit universe there is no room for compromise or cooperation.

None of this is to say that we should naively buy into the EU’s discourse that trade integration is an unquestionably good thing, or fall into facile pro-free trade arguments that see free trade as desirable at any cost and unquestionable win-win. It’s more complicated than that as the example of the ‘DMEs’ mentioned above shows. As I recently argued in an essay, EU integration has no doubt had various negative effects – e.g. the pressure it puts on wages and trade unions in some countries – as well as positive ones. Regarding the SM specifically, there are indeed fundamental problems with its construction especially since the introduction of the Euro, which has conferred export obsessed Germany an unhealthy advantage compared to other Eurozone countries that have lost the ability to devalue their currency against the Deutschmark.

Yet, regardless of these real flaws, concerning the British debate, the fact is that none of the figures analysed by Facts4EU provide any convincing argument that SM membership had a negative impact on the country’s economy and Brexit was therefore the right decision. Partly that is because, like during the referendum campaign, pro-Brexit arguments do not tell us what they are comparing EU membership to. In the case of trade, the Brexit choice is not and never was about free trade or no free trade. It is about whether we trade primarily with EU countries based on a set of not perfect, but still relatively well-developed standards regarding animal welfare, the environment, etc. or whether we rely on Liz Truss signing new FTAs with countries like Australia with very little parliamentary scrutiny.

Most importantly, though, the Facts4EU article and the Express’s reporting on it constitute yet another striking example of how Brexit was based on lies. Contrary to John Rentoul’s argument in the Independent this week, I am of the view that it is of crucial importance to avoid further damage to the British democracy that people continue pointing that out and that we try and make sure that the liars do not get away with it.